Introduction

Superalloys are special metal mixtures designed to perform under extreme heat and stress. They play a crucial role in aerospace engines, gas turbines, and power plants. As industries demand higher efficiency and durability, the superalloys market is expanding rapidly. In this article, we dive into the market’s current size, key growth drivers, segmentation, regional trends, challenges, and future outlook. By the end, you’ll understand why global superalloys growth matters for manufacturers, investors, and policymakers. Let’s explore the strength behind these high-performance alloys and the insights shaping their industry.

Superalloys are high-performance materials engineered to withstand extreme environments characterized by high temperatures, mechanical stress, and corrosive elements. Comprising primarily nickel, cobalt, and iron, these advanced metal alloys demonstrate outstanding resistance to oxidation, thermal creep, and fatigue. Their structural integrity and reliability make them indispensable across demanding sectors such as aerospace, power generation, marine, automotive, and medical applications. As innovation accelerates and industries pursue more durable and efficient materials, the superalloys market continues to evolve.

Source: https://www.databridgemarketresearch.com/reports/global-superalloys-market

Market Size and Forecast

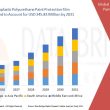

The global superalloys market was valued at USD 6.99 billion in 2024 and is projected to grow to USD 17.75 billion by 2032, at a compound annual growth rate (CAGR) of 12.4% during 2025–2032 fortunebusinessinsights.com. Another analysis reports the market reached USD 7.39 billion in 2023 and is expected to hit USD 12.06 billion by 2030, growing at 7.24% CAGR from 2024 to 2030 maximizemarketresearch.com. These forecasts show strong demand fueled by aerospace, energy, and industrial sectors needing materials that withstand high temperatures and corrosive conditions.

Key Growth Drivers

Several factors are propelling the superalloys market forward:

- Aerospace Demand: Modern jet engines seek lighter, stronger components to improve fuel efficiency and reduce emissions. Superalloys meet these needs withstanding temperatures above 1,000 °C.

- Power Generation: Gas turbines in power plants require blades and disks that resist high thermal stress for reliable electricity supply.

- Industrial Gas Turbines: Oil and gas exploration, as well as marine propulsion, rely on durable materials in harsh environments.

- Automotive Innovations: High-performance vehicles and racing engines use superalloys for parts that need extreme heat resistance.

- Research & Development: Continuous alloy improvements—like adding rhenium or cobalt—enhance strength and creep resistance, opening new applications.

Together, these drivers create a robust market environment where advanced metallurgical research and industrial needs align.

The Evolution of Superalloys

The genesis of superalloys dates to the mid-20th century when aviation and industrial sectors required heat-resistant metals for next-generation engines. Early nickel-based variants laid the foundation for aerospace applications, offering unprecedented stability under thermal stress. Through systematic alloying and metallurgical breakthroughs, subsequent generations improved creep strength and oxidation resistance. Recent developments—including powder metallurgy and additive manufacturing—have pushed boundaries further, allowing precise control over microstructure and geometry. These technological strides have broadened superalloy usage from aerospace turbines to biomedical implants and nuclear power components.

Market Trends

Aerospace & Defense Expansion: Aircraft manufacturers remain the principal consumers of superalloys due to the rising demand for efficient jet engines and lightweight airframes. The need to enhance fuel efficiency and engine performance underpins this demand.

Sustainable Processing & Recycling: Environmental concerns have led to growing adoption of recycling initiatives within the industry. Efficient reclaiming of superalloy scrap minimizes waste and reduces reliance on rare and costly raw materials.

Advent of Additive Manufacturing: 3D printing technologies enable the production of intricate superalloy components with reduced material wastage and shorter lead times. Aerospace and medical device manufacturers are leveraging this trend for customized parts.

Power Sector Growth: The need for high-temperature alloys in turbines used for fossil, nuclear, and renewable energy generation continues to rise. Superalloys are crucial to improve efficiency and lifecycle of energy systems.

Medical Sector Innovation: Increasing preference for biocompatible and corrosion-resistant implants is driving superalloy demand in orthopedic and cardiovascular treatments. Titanium-aluminum-vanadium and cobalt-chromium alloys offer durable solutions in clinical use.

Challenges

Cost-Intensive Production: Manufacturing superalloys involves advanced refining, precision casting, and heat treatment processes—resulting in elevated costs.

Supply Chain Vulnerabilities: Dependence on geographically concentrated sources for nickel and cobalt introduces risk from geopolitical instability, logistical issues, and trade restrictions.

Material Constraints in Harsh Environments: Although resilient, certain superalloys can struggle in specific aggressive chemical exposures, prompting exploration into hybrid or protective coatings.

Emerging Competition: Advances in ceramic matrix composites and lightweight high-performance polymers pose a competitive challenge in select applications, especially where weight savings are critical.

Market Scope

Superalloys serve core functions in gas turbines, aircraft engines, nuclear reactors, oil and gas equipment, marine propulsion systems, and surgical tools. North America and Western Europe dominate due to established aerospace and defense infrastructure. However, Asia-Pacific is witnessing the fastest growth, led by China, India, and Japan, fueled by industrialization, defense modernization, and renewable energy investments. Regulatory mandates for fuel efficiency and emission reduction further influence adoption patterns across regions.

Market Size

The global superalloys market continues to register robust growth. Industry analysts estimate a healthy compound annual growth rate (CAGR) over the next decade. The aerospace segment commands a substantial share, driven by commercial aviation recovery and ongoing defense procurement programs. Simultaneously, the energy segment—especially thermal and nuclear power—presents expanding opportunities. The confluence of R&D investments, technological scalability, and global focus on sustainability is reshaping the competitive landscape.

Factors Driving Growth

- Advanced Manufacturing Techniques: Improvements in single-crystal casting and powder metallurgy are enabling superior creep-resistant properties and customized geometry.

- Aerospace & Defense Investments: Fleet modernization programs, particularly in Asia-Pacific and the Middle East, are translating into heightened superalloy demand.

- Rising Sustainability Demands: Regulatory pressure to improve energy efficiency across sectors is encouraging the use of lighter and more durable alloys.

- Industrial Growth in Developing Economies: Infrastructure development, oil exploration, and power generation projects in emerging markets are creating new demand frontiers.

- Healthcare Engineering Developments: Increased surgeries and prosthetic applications worldwide are enhancing uptake of biocompatible superalloys.

Market Trends

Aerospace Driving Innovation: The aviation sector remains the largest end-user, utilizing superalloys for turbine blades, combustion chambers, and exhaust systems. Lightweight, heat-resistant materials are crucial as manufacturers strive for fuel efficiency and reduced emissions.

3D Printing in Component Fabrication: Additive manufacturing has redefined how superalloy parts are designed and produced. It reduces waste, shortens production cycles, and allows for complex geometries, especially in aerospace and medical fields.

Sustainable Sourcing and Recycling: Eco-conscious policies are pushing manufacturers toward recycling high-value superalloy scrap and adopting low-carbon production methods.

Power Generation Expansion: As nuclear, gas, and solar thermal power installations grow, demand for superalloys in turbine systems and heat exchangers is surging due to their long operating life and temperature resilience.

Growing Medical Applications: The need for biocompatible and corrosion-resistant materials is boosting the use of superalloys in orthopedic implants, dental prosthetics, and surgical tools.

Challenges

High Cost of Production: Superalloys require advanced refining processes, costly alloying elements, and strict quality control, raising the overall price tag for manufacturers and end-users.

Volatile Raw Material Supply: Global dependency on nickel and cobalt—often sourced from politically sensitive regions—adds uncertainty to the supply chain and contributes to price volatility.

Processing Complexity: Manufacturing superalloys can involve multiple heat treatments, precise casting, or welding techniques, which present technical barriers, especially in emerging markets.

Emerging Competitors: Ceramic matrix composites and high-entropy alloys are attracting attention as viable alternatives in applications where weight, cost, or corrosion pose constraints.

Future Trends and Innovations

Looking ahead, several trends will shape the global superalloys growth:

- Additive Manufacturing (3D Printing): Enables complex component designs, reduces waste, and shortens lead times.

- Alloy Recycling: Recovering nickel and cobalt from scrap to reduce costs and environmental footprint.

- Advanced Coatings: Thermal barrier coatings combined with superalloys extend component life in extreme heat.

- Digital Twin Technology: Simulating alloy performance in virtual environments to optimize design and maintenance.

- Green Manufacturing: Lower-carbon forging and melting processes to cut greenhouse gas emissions.

By embracing these innovations, manufacturers can improve performance while meeting sustainability targets.

Conclusion

The superalloys market stands on the brink of strong expansion, moving from USD 6.99 billion in 2024 to USD 17.75 billion by 2032 at a 12.4% CAGR, driven by aerospace, power, and industrial needs fortunebusinessinsights.commaximizemarketresearch.com. Nickel-based alloys and aerospace applications lead the way, while North America and Asia Pacific dominate regionally. Challenges like raw material costs and complex manufacturing push the industry toward recycling, additive manufacturing, and greener practices. As high-temperature performance and durability remain critical, superalloys will continue to underpin innovations in flight, energy, and beyond. Understanding these industry insights helps stakeholders navigate opportunities and invest in long-term growth.